Small Business Health Insurance in Florida

This guide was created to help independent professionals and small business owners provide their employees with the healthiest, most affordable benefits. It is possible to stay competitive without sacrificing the overall benefits package and compensation you offer.

Benefits Options for Small Business Health Insurance in Florida

If you own a small business in Florida, there are several options for providing employee health coverage.

Implementing a traditional plan of group health coverage is by far the easiest, most affordable option.

Prices are dependent on age. However according to figures from the Kaiser Family Foundation a worker’s and their family’s average cost for employer-sponsored insurance in 2021 is $21,184.

Florida employees contribute an average of more than $ 6,366, towards their healthcare costs.

Florida companies also have a number of options that could reduce their expenses significantly. These include:

- HSAs are health-savings accounts.

- The Health Reimbursement Arrangements (HRAs)

- Memberships in direct primary care

- Shared health care programs

The right strategy for small businesses is dependent on many factors. These include the size of your firm, budget available, as well as age, medical needs, and other requirements, of both your staff and those of their families.

Read on the go, download our Complete Guide To Small Business Healthcare Plans.

Request a Group Quote for Your Company

A Geographical Perspective for Small Business Health Insurance in Florida:

Florida is a state with a very unique health care environment. It includes large cities, such as Miami, Tampa, Orlando, and smaller towns, like Micanopy and Everglade City.

Florida businesses should carefully consider the distribution of their staff across the state. If the company’s headquarters is located in Miami, it does no good to pick an HMO plan that only allows workers to see doctors within its network. However, many employees live and/or work in Live Oak.

Florida Small Business Group Health Insurance

Most Florida employers choose traditional group health insurance.

However it may not be the cheapest.

How Small Business Health Insurance in Florida it works

Employers contract with third party insurance providers – typically a profit-making corporation – to offer a package of benefits in health insurance for employees and, if desired by the employer, their family members.

The Affordable Care Act requires that employers who have 50 employees or more offer ACA qualified health insurance for all their employees working more than 30 hour per week. Otherwise, they will be penalized.

Health insurance plans must include the 10 minimum essential coverages required by the Affordable Care Act. The ten essential coverages (MEC) are as follows:

- Patients can receive ambulatory services without needing to go into hospital.

- Emergency services

- Hospitalization can include overnight hospitalizations and surgery.

- The care of newborns, pregnant women, and mothers (both before and afterwards)

- Treatment for substance abuse disorders, mental illness and behavioral problems (including counseling and therapy)

- Prescription drugs

- The Rehabilitation and habilitative Services and Devices (services and equipment to assist people with disabilities or injuries in gaining or recovering mental and physical abilities)

- Laboratory Services

- Chronic disease management and prevention services

- Adult dental coverage and adult vision insurance are not considered essential health benefits.

ACA mandates that insurance policies cover contraception and breastfeeding.

Although traditional health insurance may be the most expensive choice for your business, you will have guaranteed enrollment.

When a worker enrolls, whether it is during the initial enrollment period or a subsequent special enrollment period due to a qualifying event in their life, or even during the November 1st open enrollment season, an insurance company cannot refuse coverage or charge them a higher rate because of medical records.

Florida Small Businesses Have the Option to Purchase Health Insurance

Employers with less than 50 employees are exempt from offering health insurance.

Florida law does not have any requirements. You don’t need to provide health insurance if you employ fewer than fifty people.

No penalty will be charged.

Employers of all sizes should consider offering health benefits. That includes very small firms, because they may find it difficult to hire and keep quality employees if there is no competitive benefit.

Florida has a low rate of unemployment and employers are fiercely competing for the best talent

Florida employers may save significant money by providing a health-sharing plan or medical cost-sharing program (more information below) and paying some of or all the employee’s costs.

HRA Alternative for Small Business Health Insurance in Florida

You can also offer your employees a QSEHRA (Qualified Small Employer Health Reimbursement Arrangement) that allows them to pay their individual health insurance tax free.

This allows workers to receive any subsidy they qualify for as part of the Affordable Care Act. This could reduce your costs as an employer because you are not paying for your workers’ entire premium plus local administrative fees, but instead the lower subsidized rates that your employees qualify for on the individual or family market via the Obamacare Exchange established in your state.

Florida’s taxation of employer health benefits

According to federal law as well as Florida state legislation, health insurance premiums are fully deductible as a business cost. Additionally, the premiums paid by employers are tax-free for employees.

They have lower total costs. They are also deductible by the employee. But employer contributions to health cost sharing are also taxable for the employee.

Florida Employer group health insurance coverage: What are the disadvantages?

Both employers and workers have important advantages to traditional group health plans.

- Cost. As mentioned above, providing health insurance at a monthly price can be prohibitive.

Some of the reasons why traditional health care insurance is so expensive are due to overkill. Washington, Tallahassee and Washington regulators have loaded health insurance plans with requirements and mandatory coverages which do not make sense for many workers.

Some traditional insurance policies include mental health benefits, drug and substance abuse coverage, as well as maternity coverage that most workers are not interested in.

The result is that they are much less effective and economical than needed.

- Inflexibility. Many group health insurance programs are a one size fits all strategy. This may not be able to adequately meet the budget and needs of each employee. Group health insurance programs sponsored by the employer tend to be one-size fits all and may not adequately address specific employee needs or budgets.

Some workers may find it more cost-effective to purchase their own health insurance plan through the private market, taking advantage if possible of the Affordable Care Act’s subsidy.

Below are some alternatives to health insurance that may be less costly. They can also be an excellent solution for those who have no health conditions and are otherwise in good health.

Below, we discuss health sharing plans in greater detail.

- Administrative burden. Administrative costs are high when managing a comprehensive health plan. It involves managing documents and compliance, auditing the plans to make sure employees are not enrolling non-qualified individuals into the plan and answering questions from staff. This is essential for a health insurance plan to run smoothly within an organization.

They are a burden for very small companies who do not have enough employees to support a full time HR team to manage the plan.

Business owners may also use strategies like Health Reimbursement Arrangements or health care stipends.

They encourage them to take out their own policies through Affordable Health Care Act. It is possible that workers can benefit from subsidies. It takes the employer completely out of the equation, saving them administrative and overhead expenses.

Health Sharing Plans for Small Business Health Insurance in Florida

Florida’s small businesses can find health sharing plans to be a cost-effective and affordable alternative to the expensive coverage of traditional insurance.

Florida businesses increasingly use medical cost sharing programs as a cheaper alternative to the traditional group health plans. Switching from group health insurance plans to medical cost sharing can result in a 50% reduction on the premiums.

Florida Small Businesses could save over $10,000 per annum per employee in family coverage and up to $3,500 annually for single coverage.

These programs represent a revolutionary method of financing healthcare. This allows companies to afford high-quality medical care for their staff while also controlling expenditures. A health sharing program is based on sharing resources across several people and organizations.

As an alternative to traditional health insurance that involves payment of premiums, the participants in a Health Sharing Program make a set amount of cash per year.

Health Sharing Plans vs. Health Insurance

The health sharing plan is not the same as health insurance.

Health sharing groups are associations made up of people with similar interests who share medical costs. Health sharing organizations are not-for-profit, unlike health insurance companies.

Mandatory Coverage

Health insurance plans don’t have the same requirements. While state and federal laws require health insurance to cover many things people do not want, or need. These requirements do not apply to health-sharing organizations.

The cost of treatment for drug addiction is not covered by medical cost sharing plans for those who do never take drugs. The plans do not have to cover injuries that result from drunk driving.

Pre-existing Conditions

Contrary to traditional health plans, some health sharing plans impose waiting period before they share costs for treating pre-existing health conditions.

These plans often impose a waiting period for surgery, unless the injury or accident was not anticipated at the time of enrollment.

Health sharing organizations can offer a wide range of services at a fractional cost of a standard ACA group health plan.

Note: Plans that offer health sharing do not qualify as subsidies under the Affordable Healthcare Act. Even if you qualify for an Affordable Care Act subsidy and switch to a health sharing program, many people will still save money.

Florida employers are often more inclined to switch from small group insurance plans that receive a subsidy for premiums under the ACA.

Request a Group Quote for Your Company

Health Sharing and Network Restrictions are in Florida

Health sharing plans offer more choices when choosing healthcare providers than traditional managed care plans like HMOs or PPOs. These are the two most popular employer sponsored group health insurance policies.

Most health sharing organizations Florida does not limit patients to only in-network providers. Members of health-sharing plans can select their doctor. People should be able to choose the doctors they want.

Are You a Business That Can Benefit From Health Sharing?

Every business has its uniqueness. The best plan to use, be it a group health plan with a traditional approach, or health sharing, requires careful evaluation.

Good news for Florida-based business owners: it is easy to obtain a case study and specific recommendations tailored to your team and organization.

You can make an online appointment by simply clicking Click Here.

It will help if you have an employee census prepared.

In most cases, switching to health insurance will save thousands of dollars per covered employee. But health sharing may not be indicated if you have workers with pre-existing conditions.

The consultation and analysis is always free.

HRAs for Small Business Health Insurance in Florida

Health Reimbursement Arrangements (HRAs) are employer-funded benefits that provide tax-free reimbursement to employees for individual healthcare costs.

Florida’s small business owners often drop group health benefits altogether. They instead establish an HRA and provide the money to their employees to purchase individual health insurance on the market with dollars pre-taxed.

The company can also benefit from the available subsidy, reducing costs for both the employee and the employer.

After paying for the insurance premiums, workers may use any remaining HRA funds to cover other costs, such as prescriptions and durable medical devices, copays or deductibles. HRA benefits remain tax-free for the employee.

When you offer an HRA as an alternative to a formal plan for group health coverage, employees have the option of choosing the insurance that meets their specific needs.

Click here to learn more about HRAs for small businesses.

HRA for Small Businesses (QSEHRA)

QSEHRA or the Qualified small employer health reimbursement arrangement (pronounced “Cue Sarah”) is available to small businesses.

It is available to companies that have fewer than fifty full-time workers or an equivalent number, but do not provide a group health plan.

The QSEHRA allows businesses to choose their maximum QSEHRA contribution, subject to certain restrictions. Florida employers may contribute $5,850 to an individual employee up to $487.50 a month and up to $11,800 to employees who have a family up to $983.33.

These employees can then use their money to get insurance for themselves via the internet health insurance exchange. Or they can buy it through a broker, who is able to offer individual or family health coverage. In this way, employees can keep their subsidy eligibility.

The employer can decide to pay the employee’s premiums for health insurance only, or also reimburse them for any extra medical expenses.

QSEHRAs and Special Enrollment Periods

If you decide to replace your current health insurance with an HRA and cancel the old plan, then your employees qualify for Special Enrollment. It is a window of 60 days during which employees can buy their own ACA approved insurance with guaranteed approval rights without going through any medical underwriting.

You can ensure that employees will not be left unprotected when you replace your existing group health insurance with the QSEHRA.

HRA Advantages

Health Reimbursement Arrangements are a great way to save money.

The money you spend for HRA benefits is tax deductible by you and tax free to your employees.

HRA funds are yours until they’re actually paid out to employees. You can use it as working capital. It is not required to be deposited with a third party.

The HRA benefit can be designed by employers in a way that suits their needs, and includes what costs you’re willing to cover.

The workers’ health coverage is not affected if they change their status to contractor or leave the organization. The QSEHRA allows the employee to control and own their insurance. The employee, not the employer.

HRA Disadvantages

Many workers do not wish to take on the task of researching and selecting their own healthcare plan. Some workers need assistance to help them navigate through the change.

We can help if you are in this situation. There is no one left behind.

Call 800-913-0172 or have your workers simply click on this link for an appointment to receive personalized service.

Learn more by clicking here about other options to the employer-sponsored insurance that Florida small businesses can choose.

The Direct Primary Health Care Advantage

Direct Primary Care plans are a new alternative to traditional healthcare. They’re gaining in popularity across Florida. This is a model based on membership: Your employees can receive as many consultations as they require, whether in-person or through telehealth, for an affordable flat monthly fee.

Membership-based: For a monthly flat fee that is affordable, similar to a gym subscription, you can provide your employees with as many appointments as needed, in person or by telehealth.

DPC memberships start as low as $80.00 per month, making it a very affordable and attractive option to improve your health.

DPC offers members access to all routine, primary, preventive and chronic health care services.

The following are some examples of direct primary healthcare services:

Some of the most common medical services offered by doctors who practice Direct Primary care include:

- Preventive care. DPC doctors are committed to preventive care and offer routine screenings, immunizations and checkups.

- DPC Doctors treat injuries and illness that are acute, such as minor cuts, infections, skin diseases, colds or flu.

- Chronic Disease Management DPC doctors assist patients in managing chronic conditions such as hypertension or diabetes. They also help with asthma and other joint problems. These doctors offer ongoing treatment, monitor patients, and adjust their plans of care as required.

- Comprehensive physical exams. DPC doctors provide comprehensive physical examinations that help assess health overall, identify possible risks, and offer personalized health recommendations.

- Urgent care. DPC is often able to offer same-day, or the next-day, urgent care.

- Services in diagnostics and laboratories. DPC specialists may provide or coordinate laboratory testing, such as electrocardiograms(ECGs), X-rays/ultrasounds/blood tests.

- Medication Management DPC doctors prescribe medication and can monitor effectiveness. They also make necessary adjustments. These doctors can also educate and counsel patients on how to use medications.

- Mental health services DPCs provide mental health treatment as a part of the comprehensive care they offer. DPC practitioners may refer to mental specialists, provide counseling or therapy.

- Minor procedures. DPC physicians are sometimes trained to do minor procedures right in the office. These include suturing lacerations and removing skin lesions or moles. They can also perform joint injections.

- Referrals to specialists and hospitals. DPC doctors serve as patient advocates, coordinating care with hospitals, other healthcare providers and specialists when referrals to them are needed.

The appointment system allows patients to be seen quickly for medical problems that are not emergencies.

No insurance companies are involved so there aren’t any co-pays. A monthly subscription will cover all costs. So, workers with limited funds can receive immediate medical attention. Never again will workers have to avoid seeing their doctors because they cannot afford the copay or the deductible.

Patients can select supplemental plans to cover additional services, such as accident insurance, high-deductible health plans or health sharing plans. DPC members can choose to cover routine health care at a lower cost by opting for health sharing plans instead of traditional insurance.

HSAs for Small Business Health Insurance in Florida

The HSA (Health Savings Accounts) is a powerful tool that can assist workers in managing their health care costs and also help to keep the premiums of workplace health insurance lower.

Florida’s residents and business owners need any tax relief they can find. Employer contributions to Health Savings Accounts for employees are fully deductible from Florida Corporate Income Tax as a compensation cost.

HSAs allow individuals to set money aside before taxes in order to pay for medical expenses down the road. HSAs are open to both employees and employers, subject to a limit set by Congress to reflect the rising cost of living.

The money in an HSA grows tax deferred, and any withdrawals made to cover qualified medical expenses are tax free.

HSA Eligibility

To qualify to make contributions or benefit from employer-paid pretax contributions, an employee must sign up for a high-deductible plan.

In 2023, an IRS-defined high-deductible healthcare plan will be any health insurance plan which has a deductible that is at least $1,500 or $3,000, depending on whether it’s for a single person or a family.

In 2023, an IRS-defined high-deductible healthcare plan will be any health insurance plan which has a deductible that is at least $1,500 or $3,000, depending on whether it’s for a single person or a family.

What if I Want To Combine HSAs or Health Shares for My Small Business Health Insurance in Florida?

At present, there is only one plan that allows employees to contribute pre-tax money into a Health Savings Account: the HSA Secure Plan. It’s available via HSA For America.

HSA SECURE Plan offers a great way to combine tax advantages and savings on healthcare with health sharing.

Your employees will need to have some income from their own business or self-employment for them to be eligible.

HSA SECURE plans are not offered to employees who receive a W-2. HSA Secure is available to employees who are self-employed, have side businesses, do freelance work, or own a business. If they’re in good health and don’t need any ongoing medical care due to preexisting conditions, this plan may be the best option.

As a small-business owner, you may want to consider the HSA Plan SECURE as an option that can save both your and partners money.

HSA SECURE is only available to employees who enroll on their own. If they already have an HSA established, then you can still make pretax contributions on their behalf up to the limit Congress sets each year.

How Are Benefits for Small Business Health Insurance in Florida Taxed?

You now know about the different strategies that small businesses can use to supplement traditional health coverage. Below is a quick table explaining each benefit’s taxation.

Plan Type Employer Workers

Traditional health insurance premiums Tax deductible. May qualify for a tax credit (see below) Non-taxable

HSA contributions Tax deductible

Pre-tax, up to certain limits. No income limitations.

Health sharing costs Tax deductible as a compensation expense Taxable as ordinary W-2 income

Health reimbursement arrangements Tax deductible Benefits are non-taxable to the employee

HSA withdrawals N/A

Withdrawals for qualified medical expenses are tax-free. Otherwise taxable as ordinary income.

A 20% penalty for non-qualified withdrawals applies up until age 65.

Direct primary care costs

Tax deductible as a compensation expense Taxable to the employee

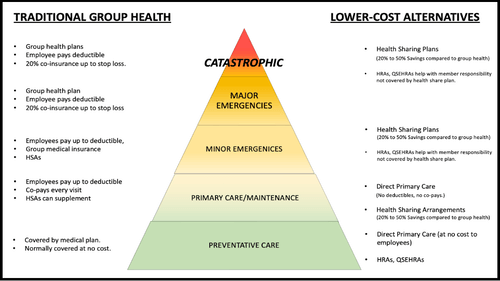

All Levels of the Care Pyramid Should be Addressed

A good employee health benefits package should address all levels of the Employee Healthcare Pyramid—from routine preventive care, through primary care access for maintenance and early detection of health problems, all the way through catastrophic incidents, as shown below:

On the left of this diagram we list common traditional insurance-based solutions that address each level of the Care Pyramid.

While on the right, we list several alternatives, more affordable approaches to providing meaningful protection for employees at each respective level of the Pyramid.

A good plan design provides employees with affordable solutions at each of these levels, so that no employee needs to delay or go without care because they can’t afford a premium, coinsurance, or copay.

Your Personal Benefits Manager can help you create a custom plan design for your work force that provides a solution at each level of the Care Pyramid – often at a fraction of the cost of a traditional group plan to the employer.

Small Business Health Insurance in Florida Tax Credit

Small Business Health Care Tax Credit enacted along with ACA is a credit that allows for some small businesses up to 50% federal tax credits on employee health insurance.

It is tailored to small companies with fewer than 25 staff members who often hire low-wage employees.

For-profit as well as non-profit organizations can both claim credit.

* You have fewer that 25 employees, and the average salary is around $53,000. (Not including all owners’ salaries). When calculating average salaries and the number employees, the owner is generally excluded. Also, “fulltime equivalents (FTEs)” are used to determine the number of workers. It means that 2 half-time employees are equal to 1 full-time employee.

* You must pay at least half the amount of your employees’ premiums.

The Affordable Care act-qualified insurance coverage is available in the Florida exchange, which is Healthcare.gov.

When an employer has at least 25 employees and/or a wage average of more than $53,000, they are no longer eligible for the tax credits.

What is the process for claiming credit?

This tax credit can be claimed on your income tax returns with IRS Form 8941 attached (tax-exempt businesses are required to submit a Form990-T to make a claim even though they do not have to).

Contributions to health insurance for your employees do not attract tax.

My business has not paid any taxes for this year. Can I claim my tax credit even though I don’t owe any taxes this year?

Yes. You can carry back the tax credit to use it to offset the income tax liability for the year before or you can carry forward the tax credit to use it to offset the liability over the following 20 years.

You can get a refund if you have a tax-exempt company.

Contact your tax advisor to learn more about the Small Business Health Care Tax Credit.

Combining Strategies for Small Business Health Insurance in Florida

Combining multiple programs may be an intelligent move to maximize health coverage.

Many employers find that they can reduce their costs by offering a range of packages to cover all employees’ needs, and still provide a comprehensive healthcare package.

You could combine Direct Primary Care Plans (DPCs), for the normal care of primary patients, with health plans that are low-cost and cover catastrophes.

Comparing this to the conventional health care insurance for groups, it can save money for you, your employees or both.

Giving employees the opportunity to select between an HDHP HDSA plan and a health-sharing plan as well as the ability to contribute money into a Health Savings Account can provide them with more flexibility.

You Have to Do Something Now

Please contact us if you would like a complementary, complimentary business health plan and analysis.

The HSA for America Benefits Manager you are connected to will discuss with you your workforce and family, budget needs and your employee’s ability to pay, as well as any existing conditions that need to be taken into consideration when creating a new program.

Many of the PBMs we work with are also successful businessmen and entrepreneurs. The PBMs understand the needs of business owners and know what is required to retain and recruit top talent.

Do I have to offer health insurance AND health sharing together?

It is possible to offer the two options together, and let employees choose what plan best fits their needs.

You may fall short of the required minimum rate of participation if you have too few employees participating in a health plan. HRAs can be used to reimburse employees for their individual health coverage, which is close to that cost.

Florida Small Business Health Plans Frequently Answered Questions

What is the Difference Between Health Insurance and Healthsharing for Small Businesses?

A health sharing plan involves members pooling their funds together to cover medical expenses.

Health Savings Accounts (HSAs) can help Florida workers manage their medical expenses?

HSAs enable individuals to pre-tax save money for future medical bills. Employers and employees both can contribute. This provides tax benefits as well as potential savings in healthcare costs.

In Florida, can employers make contributions to the HSAs of their employees?

Employers can contribute to HSAs of their employees, but only up to the annual limit set by Congress.

In Florida, can employer contributions to HSAs be claimed as a deduction from the state’s income tax?

Yes. In Florida, employer contributions to employee HSAs can be deducted from the state’s income tax.

Offer Direct Primary Care Plan (DPC) along with other insurance coverages make sense to small businesses in Florida

Combining DPC plans with other low-cost health coverage options, such as Health Sharing Plans, can result in comprehensive and cost effective healthcare solutions for businesses.

If a Florida business does not owe any taxes, can it still claim the Small Business Health Care Tax Credit?

The Small Business Health Care Tax Credit may be used to reduce income taxes owed in the prior year. It can also be carried forward up to 20-years.

What is an HRA (Health Reimbursement Arrangement) and how does it work?

An HRA is an employer-funded account that reimburses employees for qualified medical expenses not covered by their insurance plan. Employers determine what expenses are eligible and contribute funds accordingly.

HRAs can be combined with other options for coverage, such as health sharing plans and individual health insurance policies.

HRAs are compatible with other insurance options. HRAs can be used to reimburse employee premiums on individual policies. HRA funds cannot be used directly to reimburse employees for the costs of health sharing plans.

What are the waiting periods on pre-existing condition plans?

There may be a waiting period for certain healthsharing plans before the coverage is provided. You should review plan guidelines, or speak to a Personal Benefits manager for additional information.

How do I apply for the Small Business Health Care Tax Credit?

Businesses that earn a profit can claim this tax credit by filing IRS Form 8941, while businesses which are exempt from tax must file IRS Form Form990-T.

HSA for America cannot provide you with tax advice. Employers are encouraged to speak with their accountants for more details about how they can claim the credit.

What health insurance plans cover pregnancy benefits in Florida?

Florida health plans that offer health coverage and insurance often include maternity care benefits. These cover prenatal care and care during labor and delivery, as well as postnatal care. Some plans that offer health sharing may restrict cost-sharing for children conceived out of wedlock.

How do I know which health insurance options and cost-sharing plans are best for my Florida business?

It’s not a solo trip, take a team with you. Contact a Personal Benefits Manager who can conduct a free analysis and recommendation based on your specific needs, budget, employee census, and any pre-existing conditions that need to be considered. These professionals can assist in designing an optimal plan, which will help you maximize your employee’s benefits while also controlling costs.

Are there restrictions on how large a small business can be to qualify for the Florida Small Business Programs?

Only employers with fewer than fifty employees are eligible for the Qualified Small Employee Health Reimbursement Arrangement. If you employ more than fifty employees or if your business grows, you may be eligible for other HRAs.

You must also comply with the ACA’s requirement that your company provide a plan which is qualified for health coverage to its employees. Otherwise, you may be subjected to a financial penalty. You should speak to your Personal Benefits Coordinator if your company is about to or plans on hiring its 50th full time worker, or equivalent, in the next few months. Your plan could be affected.

Read More About Group Health Insurance Options in Your State

Available Plans | HSA Info | Healthshare Info | FAQS | Blog | News | About Us | Contact Us | Privacy Policy | Agents Needed

Contact Information:

1001-A E. Harmony Rd #519 Fort Collins, CO 80525

800-913-0172

info@HSAforAmerica.com

Disclaimer: All information on this website is relayed to the best of the Company's ability, but does not guarantee accuracy. Information may be out of date. The content provided on this site is intended for informational purposes only and does not guarantee price or coverage. This site is not intended as, and does not constitute, accounting, legal, tax, and/or other professional advice. Determination of the actual price is subject to the Carriers.