Idaho Small Business Health Insurance Options

The HSA for America Guide to Idaho Small Business Health Insurance. This guide is aimed at companies in Idaho with 30 or less employees.

This document is intended to help small business owners, freelancers, and independent professionals provide the best; most cost-efficient set of employee health benefits possible. So you can stay more competitive, while still offering the benefits and overall compensation package you need to attract the best available talent and keep them on the job.

Idaho Small Business Health Insurance Benefits

Idaho’s small businesses have many choices when it concerns providing employee health coverage.

It is the easiest, most affordable option to go with a traditional health care plan.

Prices are dependent on age. But according to information from the Kaiser Family Foundation, the cost of group health coverage offered by an employer that covers a family member and worker will average out at $19,788.

Idaho workers typically pay more than $6,315, or almost $150 above average, towards their health insurance.

Idaho Businesses have also a number of options to reduce their costs. These options include:

- Health savings Accounts (HSAs)

- Healthcare reimbursement arrangements

- Direct primary Care Memberships

- Health Sharing Programs

Many factors determine the best small business strategy, including your budget and size, but also your workers’ age and health requirements.

Read on the go, download our Complete Guide To Small Business Healthcare Plans.

Request a Group Quote for Your Company

Idaho Small Business Health Insurance Geographical Issues

Idaho’s healthcare landscape is unique, with both urban centers like Pocatello, Boise, Coeur d’Alene and rural towns like Riggins or Moyie springs.

Idaho employers should consider carefully how to distribute their employees throughout the state. The executives of a company headquartered in Pocatello may be tempted to select an HMO which restricts employees to only seeing doctors in the network, yet a majority of their staff and family members live and work far away from that plan.

Idaho Small Business Group Health Insurance

In Idaho, most employers opt for traditional group insurance.

It is also quite pricey.

The following is how the system works:

-

Third-party health insurers, which are usually for-profit corporations, provide benefits to employees as well as their families if they so desire.

-

According to the Affordable Care act, employers with at least 50 workers must provide ACA health insurance coverage for their full-time employees.

Health insurance plans must include the 10 minimum essential coverages required by the Affordable Care Act. The ten essential coverages (MEC) are as follows:

- Ambulatory Patient Services (outpatient services you receive without having to be admitted into a hospital).

- Emergency services

- Hospitalization is a term used to describe a hospital stay (such as surgery or overnight stays).

- Care of the newborn, both before and after delivery, as well as pregnancy, maternity, and maternity care

- Services for mental health disorders and addictions, such as counseling and psychotherapy.

- Services related to mental health, substance abuse disorder and behavioral health (such as psychotherapy and counseling)

- Prescription drugs

- Services and Devices for Rehabilitation and Habilitative (Services and Devices to Help People with Injuries, Disabilities, and Chronic Conditions Gain or Recover Mental and Physical Skills)

- Laboratory services

- Services for prevention and wellness and management of chronic diseases

- Children’s services including dental and eye care are covered (adult dental and visual coverage is not essential).

The ACA also requires that health insurance cover birth control and breast-feeding.

The traditional option of health insurance, while expensive for companies, has the advantage that it is guaranteed to enroll.

When a worker enrolls for health insurance, whether it is during the initial enrollment period or a subsequent special enrollment period that follows a qualifying event in their life, or even during the November 1st open enrollment period, an insurer can not deny or increase premiums because of the medical history of the individual.

Idaho Small Businesses Do Not Need Health Insurance

In accordance with the Affordable Care Act employers employing fewer 50 people are not obliged to offer insurance.

Idaho has also made no requirements. The law does not require employers with fewer 50 workers to offer any type of health insurance.

The penalty is not applicable to you.

Even small businesses should offer competitive health insurance, as it can be difficult to retain and recruit quality staff without it.

Idaho is a great place to work, especially since unemployment rates are low. Also, employers compete fiercely for the best talent.

Idaho employers are able to save considerable money by offering medical cost-sharing or health-sharing plans (more details below) that pay for some or all costs.

The HRA Alternative

You can help your employees purchase individual health coverage on an taxable basis by offering a QSEHRA, which is a small employer qualified health reimbursement arrangement.

QSEHRAs provide employers with the following benefits:

1.) There are no minimum contributions

QSEHRAs do not require you to make a certain minimum amount every year like pension plans. Employers can choose their own HRA budget, which they may change each year depending on cash flow.

A QSEHRA allows you to control the budget of your medical benefits.

2.) Flexibility

If you want to discriminate, then offer a higher or lower amount depending on the marital status of your employees. If you want to discriminate, then give a larger benefit to single employees or employees with dependents. This reflects the actual costs of buying health insurance.

3.) The tax exemption is available to both employees and employers

You can deduct your contributions as compensation expenses. Contrary to cash compensation, employees do not have to pay taxes on QSEHRA benefits as long as they keep a health plan with the minimum coverages required by the Affordable Care Act.

In this case, a QSEHRA will be more effective than simply giving employees a health insurance allowance that they can use for other purposes or to pay their health insurance premiums.

4.) QSEHRAs are designed to support the employee’s choice

In many cases, traditional health insurance group plans are designed to limit employees with a variety of circumstances and backgrounds into one or two choices.

The HR department and the company’s management select these items, which are overpriced or unsuitable to workers.

A QSEHRA offers workers and families a wide range of options and gives them the power to select a health plan which is right for them.

Idaho taxed employer health coverage

As an employer, you can deduct all of the costs associated with health insurance as part of your business expenses under federal and Idaho laws. Additionally, the premiums paid by employers are tax-free for employees.

The overall cost of health sharing plans is lower. Employees can deduct the monthly cost of these plans from their taxes. Employer assistance to pay health-sharing costs is taxable for the employee.

Idaho Small Group Health Insurance Coverage: Disadvantages

Employers and employees alike have some serious disadvantages to the traditional employer-group health insurance.

- The Cost

The cost could be more substantial than it has to be.

The government regulators of Washington and Boise have crammed health insurance policies full of mandatory coverages that are not practical for most workers.

A traditional health plan, for instance, includes coverages such as mental health and addiction treatment, along with drug and alcohol coverage. Many workers may not want or need these benefits. This reduces their efficiency and costs.

- Inflexibility

Most group insurance programs offer an all-encompassing strategy that does not necessarily meet employee budgets and specific needs. Typically, employer-sponsored plans for group health care tend to have only a couple of options. These may not meet the specific needs of employees.

The Affordable Care Act may offer subsidies to workers who purchase individual plans.

It may also make sense to opt for a health-sharing program, which is less expensive. Innovative and affordable health insurance alternatives can provide a solution, especially to workers in excellent health with no existing conditions.

Here’s a more detailed look at health-sharing plans.

- Administrative burden

This involves managing paperwork and compliance. Auditing plans in order to prevent employees from enrolling people who aren’t qualified, as well as responding to staff questions. It is important to perform these duties for the organization’s health insurance program to operate smoothly.

These plans are expensive for small employers, who may not be able to afford a dedicated HR person to oversee the program.

In addition, owners of businesses can use other strategies including Health Care Stipends and Reimbursement Arrangements.

The Affordable Care Act offers alternative ways to encourage people to get their own health insurance. The workers may benefit from the available subsidies. The employer is also removed from the whole process.

Idaho Health Sharing Plans

Idaho’s small-business owners have an economical and feasible alternative to high-priced medical insurance.

Idaho is seeing an increase in businesses using medical cost share plans to replace traditional group health care plans. When switching from group health coverage to medical cost-sharing, businesses can typically save almost 50% on their premiums.

Idaho Small Businesses could save as much as $10,000 per annum per employee, for family coverage and over $3,500 annually for single coverage.

These innovative programs allow employers to offer employees high-quality health care, while still controlling costs. These programs are based on the idea of sharing resources with a large group of individuals or organizations.

Participants in health-sharing programs pay an annual amount to the insurance company instead of paying the premiums.

Health Sharing Plans vs. Health Insurance

It is important to note that health share plans and insurance are two different things.

Health sharing groups are associations made up of people with similar interests who share medical costs. Health sharing organizations are not-for-profit, unlike health insurance companies.

Mandatory Coverages

Health insurance plans are not required to meet these requirements. Health sharing organizations are exempt from the Ten Essential Minimum Coverage requirements.

The cost of treatment for drug addiction is not covered by medical cost sharing plans for those who do never take drugs. The plans do not have to cover injuries that result from drunk driving.

How about prior existing conditions?

Health sharing plans can impose waiting times before sharing the cost of pre-existing medical conditions.

The waiting period for surgery is often imposed by the insurance companies, except in cases of accidents or injuries that were not anticipated prior to the enrollment.

The waiting period eliminates a lot of negative selection and allows health sharing organizations to offer a fantastic set of benefits for a fraction the price of a non-subsidized ACA qualified group health insurance plan or one bought through Your Health Idaho.

Please note that health sharing plans do not qualify for subsidy under the Affordable Health Care Act. However, the savings are so significant that even those who do not qualify for subsidies can benefit by switching to a health sharing plan.

Idaho employers often find it more cost-effective to switch from small group health plans that receive a subsidy for premiums under the ACA.

Request a Group Quote for Your Company

Health Sharing and Network Restrictions are in Idaho

Health sharing plans offer more choices when choosing healthcare providers than traditional managed care plans like HMOs or PPOs. These are the two most popular employer sponsored group health insurance policies.

Idaho’s health sharing organizations do not typically restrict access to their providers. The members of the health sharing plans have the option to pick their own physician or provider. The freedom of choice for people to choose their doctors.

Are you a business that can benefit from health sharing?

Each company is unique. Choose the plan that is best for you, be it a group health plan with a health sharing model or one of traditional insurance plans.

Business owners in Idaho can easily get an analysis of their case and recommendations that are specific to the organization they run and its employees.

We’ll get started by clicking on this link, to set up an appointment.

If you’ve prepared a census of your employees, it will make things easier.

Changing to health coverage can often save employees thousands of dollars. If you are dealing with employees who have pre-existing health conditions, it may be best to avoid health sharing.

It is always free to contact us to get your complimentary consultation and analysis.

Small Businesses in Idaho may be eligible to receive reimbursement for medical expenses

The Health Reimbursement Arrangements, or HRAs as they are also known, is a benefit funded by the employer that allows employees to receive tax-free reimbursement for healthcare expenses.

Idaho small businesses often do away with the benefit of group health insurance. Instead of establishing an HRA, the small businesses use it to give their workers cash so they can buy individual insurance with pretax dollars.

The company can also benefit from the available subsidy, reducing costs for both the employee and the employer.

After paying for the insurance premiums, employees can use any HRA funds left to cover other costs, such as prescriptions and durable medical devices, copays or deductibles. HRA benefits remain tax-free for the employee.

By offering an HRA instead of a group insurance plan that is formal, you give your employees the freedom to select health plans based on their preferences and needs.

Click here for further information on HRAs and small businesses.

HRA for Small Businesses

QSEHRA or Qualified Small Employee Health Reimbursement Agreement (pronounced “Cue Sarah”) is the special HRA type that small businesses can utilize.

This benefit is intended for businesses with fewer 50 full-time staff or its equivalent.

Business owners can set the maximum QSEHRA amount they wish to contribute, as long as it is within certain parameters. Idaho employers are allowed to make contributions up until 2023 of up $5,850 (up $487.50 monthly for an individual employee) or up $11,800 (up $983.33 for a family).

These employees can then use their money to pay for insurance themselves, either through an online health insurance exchange service or a Personal Benefits Manager. In this way, employees can keep their subsidy eligibility.

Employers can reimburse their employees either for the premiums alone or for both premiums and additional medical expenses.

Special enrollment periods and QSEHRAs

You will have to offer your workers a Special Registration Period if your HRA replaces your old health insurance. This 60 day window allows employees to choose their own ACA insurance plan, with guaranteed-issue rights.

The QSEHRA will ensure that you don’t have to worry about your employees losing coverage if your QSEHRA replaces your current group health plan.

HRA Advantages

Health Reimbursement Arrangements are a great way to save money.

The money you pay for HRAs is tax-deductible by you and tax-free for your employees.

HRA funds are yours until they’re actually paid out to employees. You can use it as working capital. It is not required to be deposited with a third party.

The HRA benefit can be designed by employers in a way that suits their needs, and includes what costs you’re willing to cover.

The workers’ health coverage is not affected if they change their status to contractors or leave the business. The QSEHRA allows the employee to control and own their insurance. The employee, not the employer.

HRA Disadvantages

Many workers do not wish to take on the task of researching and selecting their own healthcare plan. It’s possible that some workers need extra assistance to make the switch.

You can get help from your HSA for America Benefits Manager if this happens. This ensures that no worker gets left behind.

To schedule an individual appointment, have your employees Click this Link or call 1-800-913-0172.

To learn about Idaho’s alternatives to health insurance provided by employers, click here.

Direct Primary Care: The Advantage

Direct Primary Care plans, or DPCs for short, are an alternative model of healthcare that has been gaining in popularity both in Idaho and throughout the United States.

This is a model based on membership: Your employees can receive as many consultations as they require, whether in-person or through telehealth, for an affordable flat monthly fee.

DPC offers a monthly membership cost of only $80 for those who want to prioritise their health and avoid the copays or insurance co-payments.

DPC Plans provide unlimited access to primary care, chronic and preventive services.

Direct primary care services include the following:

These are the services that Direct Primary Care physicians provide:

- Preventive care. DPC physicians emphasize prevention medicine, providing services like routine checks-ups and immunizations as well as screenings and tests for different conditions.

- DPC physicians treat minor injuries and acute illness such as colds and flu.

- Management of chronic diseases DPC doctors can help manage chronic diseases like diabetes, hypertension and asthma. The doctors provide continuous care and monitoring as well as adjustments to the treatment plan when necessary.

- Comprehensive physical exams. DPC physicians offer comprehensive physical exams to evaluate overall health, identify risks and give personalized recommendations.

- Urgent care. DPC physicians are available to provide same-day and next-day emergency care.

-

Patients can receive immediate attention to non-emergency issues by making appointments.

- Diagnostic and laboratory services. DPC physicians may coordinate or offer a wide range of diagnostic and laboratory services, including blood tests, urine analyses, imaging studies, (X-rays, ultrasounds), electrocardiograms, etc.

- Management of medication. DPC doctors are able to prescribe medication, track their effectiveness and adjust as necessary. The doctors also offer education on the proper use of medications.

- Mental Health Services As part of comprehensive health care, many DPCs offer mental health services. DPC physicians may offer counseling, therapy and refer patients to specialists in mental health when needed.

- Minor procedures. Minor procedures.

- Referrals and coordination of care. DPC physicians act as advocates for patients and coordinate with other health care providers, specialists, hospitals and hospitals when necessary.

Since there is no insurance provider involved, you don’t have to worry about copays, coinsurance or deductibles. Everything is covered by the monthly subscription. The monthly subscription covers everything. This allows cash-strapped employees to get the immediate care they require. The workers will never have to delay seeing a doctor due to the cost of the co-pay or deductible.

If patients need additional coverage, they can opt for supplemental plans that include high deductible health plans (high deductible health insurance), health sharing plans (health sharing plans) or accident insurance. DPC offers routine healthcare as part of membership. Patients can select more cost-effective coverage such as health sharing plans instead of traditional health insurance.

Accounts Health Savings Accounts

Health Savings Accounts can help employees manage medical expenses and lower premiums for their workplace insurance.

Idaho businesses and residents need all the tax breaks they can get. It’s good to know that employer contributions made by employees into their Health Savings Accounts are deductible as compensation expenses from Idaho corporate income taxes.

HSAs allow individuals to set money aside before taxes in order to pay for medical expenses down the road. HSAs are open to both employees and employers, subject to a limit set by Congress to reflect the rising cost of living.

Withdrawals to pay qualified healthcare costs are tax-free.

HSA Eligibility

Employees who want to contribute to their HSA or receive employer-paid pretax contributions must sign up for an High Deductible Health Plan (HDHP).

According to the IRS, a high deductible plan is one that has a deductible at least of $3,000 for the family or $1500 for individuals.

Total annual HDHP out-of-pocket costs (including deductibles copayments coinsurance and other expenses) cannot be higher than $7500 for an individual. The limit is not applicable to outside-network providers. ).

What if I want to combine HSAs or health shares?

At present, there is only one plan that allows employees to contribute pre-tax money into a Health Savings Account: the HSA Secure Plan. It’s available via HSA For America.

HSA SECURE Plan offers a great way to combine tax advantages and savings on healthcare with health sharing.

Your employees will need to have some income from their own business or self-employment for them to be eligible.

HSA SECURE plans are not offered to employees who receive a W-2. HSA Secure is available to employees who are self-employed, have side businesses, do freelance work, or own a business. If they’re in good health and don’t need any ongoing medical care due to preexisting conditions, this plan may be the best option.

You and your small-business partners may find that the HSA Secure Plan is a fantastic way to save some money.

Employees would be required to sign up for HSA SECURE themselves. You can contribute pre-tax to their HSA once they enroll and establish it.

Click here to learn more about HSA SECURE.

How Idaho Small Business Health Insurance Benefits Are Taxed?

You now know about the different strategies that small businesses can use to supplement traditional health coverage. Here is a table that explains how these alternative health care strategies are taxed.

Plan Type Employer Workers

Traditional health insurance premiums Tax deductible. May qualify for a tax credit (see below) Non-taxable

HSA contributions Tax deductible

Pre-tax, up to certain limits. No income limitations.

Health sharing costs Tax deductible as a compensation expense Taxable as ordinary W-2 income

Health reimbursement arrangements Tax deductible Benefits are non-taxable to the employee

HSA withdrawals N/A

Withdrawals for qualified medical expenses are tax-free. Otherwise taxable as ordinary income.

A 20% penalty for non-qualified withdrawals applies up until age 65.

Direct primary care costs

Tax deductible as a compensation expense Taxable to the employee

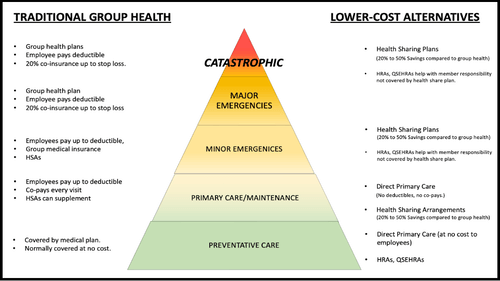

Idaho Small Business Health Insurance Pyramid

Employee health benefit packages should include all aspects of the Employee Healthcare Pyramid. This includes routine preventive health care, primary care access, early detection of problems and maintenance, right through to catastrophic incidents.

The left side of this page lists the common solutions that are based on traditional insurance and address the different levels of the Care Pyramid.

Right, you will find a list of more affordable alternatives to offer meaningful protection at every level of Pyramid.

The design of a good plan provides affordable options for employees at every level. This ensures that employees don’t have to put off or delay care for lack of funds.

You can work with your Personal Benefits Manager to create a customized plan for each employee that addresses the Care Pyramid at the appropriate level. These plans are often a fraction the price of traditional group insurance.

Idaho Small Business Health Insurance Tax Credit

Small Business Health Care Tax Credit enacted along with ACA permits certain small companies to claim a Federal Tax Credit of up to half of the costs of health insurance for their employees.

It is designed to help small businesses who employ 25 workers or less, and are also more inclined to use lower-wage employees.

For-profit as well as non-profit organizations can both claim credit.

* Has fewer then 25 employees. Average salaries are around $53,000. It is not common to include owners when determining the number and average salary of the employees in a company. The total number of staff is calculated using “full-time employees” (FTEs). The two part-time employees will equal the full-time equivalent.

Employees must be paid at least the half-cost of their insurance premiums.

Your Health Idaho is Idaho’s state exchange.

Tax credits will no longer be available to employers who have 25 or more employees or average wages of at least $53,000.

How do I claim my credit?

If you are a small business that is tax exempt, then the IRS Forms 990-T must be filed to receive this credit.

Taxes on your contributions to employee health care aren’t applicable.

It’s not true that I owe tax for my company this year. Can I still claim a tax credit?

Yes. It is possible to carry this tax credit back to offset tax liability from the previous tax year.

This credit is refundable for businesses that are exempted from paying taxes.

To learn all about the Small Business Health Care Tax Credit consult with your accountant.

You Have to Do Something Now

For the best results, you should conduct an employee survey and Contact us to receive a complimentary business health assessment and recommendation.

The HSA for America Benefits Manager you are connected to will discuss with you your workforce and family, budget needs, employee contributions, as well as any existing conditions that need to be taken into consideration when creating a new program.

Can I provide both Health Insurance and Health Sharing at the same?

If you offer both, employees can choose the one that suits them best.

Please note that if too many of your employees choose to opt out, then you may not be able to keep a group insurance plan. You can use a HRA as a reimbursement for the employee’s individual health insurance. This will cost close to the same.

Idaho Small Business Health Insurance: FAQs

What is the Difference Between Health Insurance and Healthsharing for Small Businesses?

A health sharing plan involves participants contributing money into a pool to cover medical expenses.

In Idaho, can employer contributions to HSAs be claimed as a deduction from the state’s income tax?

Yes. In Idaho, employer contributions to employee HSAs can be deducted from the state’s income tax.

Is it a good idea for Idaho small business owners to offer a Direct Primary Care plan (DPC), along with other options?

Small businesses can benefit from a cost-effective solution by combining DPC and low-cost options such as health sharing plans.

Is it possible for a business to claim the Small Business Health Care Tax Credit even if there are no taxes due in Idaho?

You can carry the Small Business Health Care Tax Credit backwards to offset your income tax liabilities from previous years or forward for up 20 years.

What is the Health Reimbursement Agreement (HRA)?

HRAs, or Health Reimbursement Accounts (HRAs), are funded by employers and reimburse employees who have qualified medical expenses which their insurance does not cover. Employers contribute to the account based on what expenses they determine are eligible.

What is the best combination of cost-sharing and health insurance for my Idaho small business?

A Personal Benefits Manager can be contacted to help you get it done. They can provide a complimentary analysis and recommendations based on the specifics of your needs, including budget, employee count, and pre-existing conditions. The experts can design a plan to maximize the value of your employees, while controlling costs. This will help you stay competitive.

Can you tell me about the waiting period for health plans that cover pre-existing conditions?

Health Savings Accounts (HSAs) can help Idaho employers manage their medical expenses.

HSAs enable individuals to pre-pay for medical costs in the future. Employers and employees both can contribute. This provides tax advantages as well as potential savings in healthcare expenses.

Employers in Idaho can contribute to HSAs for their employees.

Employers can contribute to HSAs of their employees, but only up to the annual limit set by Congress.

How do I apply for the Small Business Health Care Tax Credit

Businesses that earn a profit can claim the credit by filing IRS Forms Form 8941. However, small tax-exempt companies must file a form 990T.

HSA for America cannot provide you with tax advice. Employers can consult their own tax advisors to get full details of the credit.

In Idaho, are maternity benefits included in health sharing plans?

Idaho health plans that offer health insurance and healthsharing often include maternity coverage, which includes prenatal care, labour, and postnatal health care. Cost-sharing for children born out of wedlock may be restricted in some healthsharing plans.

HRAs work with individual and health sharing plans as well as other health coverage plans.

Yes. HRAs and other coverage options can be combined. HRAs have been used by small business owners to pay for employee policies and cancel their group insurance. HRA money is not able to be reimbursed directly by employees for costs associated with health sharing plans.

Only employers with fewer than fifty employees are eligible for the Qualified Small Employee Health Reimbursement Arrangement. If you employ more than fifty employees or if your business grows, you may be eligible for other HRAs.

You’ll also be required by the ACA to offer a health plan that is qualified for your workers, otherwise you will have to pay a fine. Speak to your Personal Benefits manager if you plan on hiring your 50th employee or the equivalent soon. This could have an impact on your plans.

Read More About Group Health Insurance Options in Your State

![]()

Available Plans | HSA Info | Healthshare Info | FAQS | Blog | About Us | Contact Us | Agents Needed

1001-A E. Harmony Rd #519 Fort Collins, CO 80525

Telephone: 800-913-0172

[email protected] | © 2024 - All Rights Reserved

Disclaimer: All information on this website is relayed to the best of the Company's ability, but does not guarantee accuracy. Information may be out of date. The content provided on this site is intended for informational purposes only and does not guarantee price or coverage. This site is not intended as, and does not constitute, accounting, legal, tax, and/or other professional advice. Determination of actual price is subject to Carriers.