Washington, D.C. Small Business Health Insurance Options

The Complete Washington, D.C. Small Business Health Insurance Guide (2026 Edition)

Welcome to the HSA for America complete guide to Washington, D.C. small business health insurance.

This guide focuses specifically on companies with 50 employees or fewer, headquartered in or having employees in Washington, D.C.

Whether you’re a small business owner, freelancer, or independent professional, providing health affordable access to healthcare can be a daunting task.

Not only is it expensive, but there are a lot of different options to choose from, and it can be hard to know which one is right for you.

That’s where we come in.

The HSA for America complete guide to Washington, D.C. small business health plans is written to help you make the best decision for yourself, your family, and if you have employees, for them and their families as well.

In this guide, we’ll cover everything you need to know about health plan options for small businesses in Washington, D.C.

Topics will include:

- The high cost of traditional group health insurance

- Health sharing—a more affordable alternative

- Health reimbursement arrangements (HRAs)

- Health savings accounts (HSAs)

- Direct primary care (DPC) plans

Read on the go, download our Complete Guide To Small Business Healthcare Plans.

Request a Group Quote for Your Company

The Problem

If you are a small business owner, freelancer, or independent professional, you know how important it is to provide your employees with quality health insurance.

Not only is it the right thing to do, but it can also be a great way to attract and retain top talent.

However, finding the right health plan for your own household or small business can be a challenge. There are a lot of different factors to consider, such as the cost of the plan, the different plan options, benefits, and exclusions, potential out-of-pocket costs, and the needs of your employees, if you have employees.

Traditional Health Insurance Coverage is Increasingly Out of Reach

Washington D.C. is an expensive place to live and work.

The cost of health insurance can be prohibitive for many District of Columbia small businesses.

According to a study from the Kaiser Family Foundation, the average annual cost of employer-sponsored group health insurance covering a worker and family in 2021 was $21,830. Out of that, Washington, D.C. employees typically contribute $6,627 on average toward their health insurance, with employers covering the remaining $15,203.

Self-employed individuals and independent contractors can pay even more, since they don’t get an employer subsidy. They are the employer!

Why is Health Insurance in D.C. so Expensive for Small Businesses?

There are a number of factors that contribute to the high cost of health insurance in the District of Columbia.

- Government regulations. Both the federal government and the District of Columbia have a number of laws and regulations that contribute to the high cost of health insurance. These regulations include the requirement that health insurance plans cover a wide range of services, including mental health and substance abuse treatment, maternity care, and preventive care—even for people who may not want or need this kind of coverage.

- Adverse Selection. The Affordable Care Act also forces insurance companies to accept all applicants who apply during Open Enrollment. They also require health insurance plans to be offered to all residents, regardless of their health status.

- High demand for health care. The District of Columbia has a high demand for health care, which also contributes to the high cost of health insurance. The District has a large population of uninsured and underinsured residents, which puts a strain on the healthcare system as a whole and drives up the cost of care throughout the greater D.C. area.

- Insurance company profits. Health insurance companies are for-profit businesses, and they need to make a profit in order to stay in business. This profit is reflected in the cost of health insurance premiums.

Thinking Beyond Traditional Health Insurance

Small businesses in Washington, D.C. have multiple health plan options when it comes to providing health benefits to employees.

Option one, the most common, is traditional health insurance—whether it’s an individual or family plan purchased over the ACA exchange, or an Affordable Care Act-qualified group plan for a small business with employees or for an association.

But of all the possible solutions, traditional health insurance is the costliest by far, except for those who receive a subsidy under the Affordable Care Act.

But traditional health insurance products are just one of several possible tools in the employers’ health benefits tool kit. Washington, D.C. businesses and independent workers also have a variety of other options at their disposal.

These include:

- Health sharing plans

- Hybrid health sharing and HSA-qualified plans

- Health reimbursement arrangements (HRAs)

- Direct primary care plans

The best strategy for small businesses depends on multiple variables, such as size, age and life stage of employees, budget, and any pre-existing conditions among plan members and their dependents, if you are including dependents in the plan.

Good plan design takes each of these factors into careful consideration, and often uses a combination of strategies, products, and solutions to provide a fuller spectrum of healthcare benefits.

Learn More: The Complete Guide To Small Business Healthcare Plans.

Health Insurance is Optional for Washington, D.C. Small Businesses

Under the Affordable Care Act, employers with fewer than 50 workers are not required to offer health insurance at all.

This is also true for Washington, D.C. businesses.

If you are smaller than 50 employees, there’s no penalty for not sponsoring a health insurance plan for your workers.

But you can still offer a meaningful benefit to your workers, and even purchase it for yourself and your family, at a fraction of the cost of an unsubsidized traditional health insurance product.

You can offer a health sharing plan, and pay some or all of the costs for your employees. This has the advantage of lower costs for your business—even if you pay the entire cost of your employee’s health sharing plan. However, the disadvantage is that any money you provide to your employees to pay the cost of the health sharing plan is a taxable benefit for your workers.

Or you can offer a health reimbursement arrangement, and help your employees pay their health insurance premiums, and possibly other medical costs, as well.

Taxation of Employer Health Coverage in Washington, D.C.

Health insurance premiums you pay as an employer are fully deductible as a business expense under both federal and Washington, D.C. state law.

The same is true of health sharing costs, and all other compensation costs: all of them are fully deductible to the employer as a business expense.

They are also not taxable to the employee.

Health sharing plans feature lower overall costs compared to traditional health insurance. Their monthly costs are also tax-deductible to the employee. However, employer assistance for paying health sharing costs are taxable to the employee.

Employer Health Benefits and Tax Treatment in Washington, D.C.

| Health Benefit | Tax Treatment for Employer | Tax Treatment for Employee | Reduces Employer Payroll Taxes? |

|---|---|---|---|

| Cash Stipends for Health Benefits | Deductible as a business expense. | Taxed as income. | No |

| Health Insurance Plans | Premiums are deductible as a business expense; not subject to payroll taxes. | Premiums paid by the employer are not taxable income; employee-paid premiums can be pre-tax if through a Section 125 plan. | Yes, if offered through a Section 125 plan. |

| Health Sharing Plans | Not typically deductible as a business expense since they're not considered insurance; depends on the structure. | Contributions are usually after-tax and not deductible. | No |

| HSAs (Health Savings Accounts) | Contributions are deductible as a business expense; not subject to payroll taxes if made through a Section 125 plan. | Contributions are pre-tax if made through payroll deduction; tax-deductible if made directly, and withdrawals for qualified expenses are tax-free. | Yes, if contributions are made through a Section 125 plan. |

| QSEHRAs | Reimbursements are deductible as a business expense; not subject to payroll taxes. | Reimbursements for qualified medical expenses are tax-free. | Yes |

| ICHRAs (Individual Coverage HRAs) | Reimbursements are deductible as a business expense; not subject to payroll taxes. | Reimbursements for qualified medical expenses are tax-free. | Yes |

| Section 125 Cafeteria Plan Benefits | Contributions are deductible as a business expense; not subject to payroll taxes. | Contributions are pre-tax, reducing taxable income; benefits received are generally tax-free if used for qualified expenses. | Yes |

| FSAs (Flexible Spending Accounts) | Contributions are deductible as a business expense; not subject to payroll taxes if made through a Section 125 plan. | Contributions are pre-tax, reducing taxable income; withdrawals for qualified expenses are tax-free. | Yes, if contributions are made through a Section 125 plan. |

| Direct Primary Care Plan Memberships | Deductibility as a business expense can vary; not typically subject to payroll taxes if structured as a health plan benefit. | Tax treatment varies; may be considered a qualified medical expense and paid with pre-tax dollars through an HSA, FSA, or HRA. | Depends on the structure and if offered as part of a Section 105 or 125 plan. |

This table provides a general overview, but specific tax treatments can vary based on how each benefit is structured and offered by the employer.

Disadvantages of Employer Group Health Insurance Coverage in Washington D.C.

Traditional health insurance products work best for individuals who get a subsidy via the Affordable Care Act for a marketplace plan, those who have an employer or the government paying most of their premium for them, and people with pre-existing conditions that need to be covered from Day 1 of enrollment.

But hundreds of thousands of D.C. residents don’t qualify for the so-called “Obamacare” subsidy, primarily because they make too much money (or, conversely, don’t have enough deductions).

You Must Pay High Premiums for Coverage You Don’t Need

Labor-intensive businesses in the District of Columbia are particularly hard-hit by the high cost of providing health insurance to their employees.

Not only are monthly premiums expensive, but the plans often come with coverage requirements that are not tailored to the needs of workers.

For example, by law, ACA-qualified health insurance plans include coverage for drug and alcohol addiction, mental health treatment, and maternity care—all of which are important, but may not be necessary for all employees.

If you don’t drink or use drugs, and you’ve never done so, and you aren’t at risk of doing so in the future, it probably doesn’t make sense for government to force you to pay extra to cover drug and alcohol rehab services.

But health insurance laws force insurance companies to cover them,. driving up the cost of coverage even further.

Lack of Choice When Shopping Group Health Insurance Plans

In addition to the high cost, traditional health insurance plans can be inflexible – especially in the employer group context.

They often offer a one-size-fits-all approach that doesn’t take into account the unique needs of individual employees.

This can lead to workers either being underinsured or paying too much for coverage they don’t need.

Too Much Paperwork

Finally, managing a group health insurance plan can be a significant administrative burden for small businesses.

It involves a lot of paperwork, compliance with regulations, and responding to employee questions.

This can be a challenge for businesses that don’t have the resources to devote to a full-time HR staff.

But there are other Options

There are a number of alternative options for small businesses in the District of Columbia that offer lower costs, greater flexibility, and less administrative burden.

These include health sharing plans and health reimbursement arrangements (HRAs).

Health sharing plans are typically less expensive than traditional health insurance products. And they don’t require employers to contribute to the cost.

HRAs, meanwhile, allow employers to set aside money to help employees pay for their health insurance premiums. HRAs are also tax-free to employees.

These alternative approaches encourage workers to buy their own insurance coverage via the Affordable Care Act.

This may help workers benefit from available subsidies. It also gets the employer out of the process altogether, reducing overhead and administrative costs.

Health Sharing Plans in Washington, D.C.

Health sharing plans are a revolutionary way to cut costs without sacrificing quality.

Thousands of North Dakota residents who’ve been left out of the Affordable Care Act subsidies as well as small businesses are saving up to 50% on premiums just by dropping traditional health insurance products and switching to health sharing.

That means you could save more than $10,000 per year for your own household or per employee for family coverage, and more than $3,500 for your own household or for each enrolled employee per year for single coverage.

Health sharing programs work by pooling resources from a group of people or organizations. When someone in the group gets sick, the costs are shared among everyone. This means that you can get the high-quality care you need without breaking the bank.

If you’re a small business owner in North Dakota, consider switching to a health sharing plan. It’s a smart way to save money and provide your employees with the healthcare they deserve.

Learn More: How Much Can Health Sharing Save?

Health Sharing vs. Health Insurance

Health sharing plans are not the same thing as health insurance.

Instead, health sharing organizations are voluntary associations of like-minded people who agree to help share the medical expenses of other members. In contrast to health insurance companies, which are usually for-profit corporations, health sharing ministries are non-profit organizations

Health sharing programs work by pooling resources from a group of people or organizations. When someone in the group gets sick, the costs are shared among everyone. This means that you can get the high-quality care you need without breaking the bank.

In addition to saving money, health sharing plans offer several other benefits for small businesses in Washington, D.C.

- They can provide access to high-quality healthcare. Health sharing plans typically have broad networks of providers, so you can be sure that your employees will have access to the care they need.

- They are portable. Employees can take their health sharing plan with them if they change jobs.

- They are flexible. Health sharing plans offer a variety of options to meet the needs of different businesses and employees.

Mandated Coverages

While federal and state laws require traditional health insurance policies to include coverage for many things that many people don’t want or need, health sharing plans have no such requirements.

The 10 Minimum Essential Coverage requirements don’t apply to health sharing organizations.

Medical cost-sharing plans are not required to cover the cost of addictions treatment for people who never use drugs, for example. And they don’t need to cover the cost of treating injuries as a result of the members’ drunk driving.

Health Sharing, Pre-Existing Conditions, and Surgeries

One of the main differences between health sharing plans and traditional health insurance plans is the way in which they handle pre-existing conditions.

With traditional health insurance plans, pre-existing conditions are typically covered after a waiting period. However, health sharing plans may impose waiting periods before they will share the costs of treating pre-existing conditions.

This is because health sharing plans are designed to be used by healthy people who are unlikely to have pre-existing conditions. The waiting periods help to protect the health sharing pool from being overwhelmed by people with pre-existing conditions.

Surgeries

Another difference between health sharing plans and traditional health insurance plans is the way in which they handle surgeries.

Health sharing plans often impose waiting periods on surgeries, except for injuries and accidents that could not have been foreseen prior to the member’s enrollment. A 90-day waiting period on non-emergency surgeries is common.

Despite these differences, health sharing plans are generally a very good option for small businesses in Washington, D.C. They offer many of the same benefits as traditional health insurance plans, but at a fraction of the cost. And, with the high cost of traditional health insurance, small businesses may find that the savings offered by health sharing plans outweigh the potential drawbacks

Health Sharing Lets You Choose Your Own Doctor

At HSA for America, we believe healthcare freedom should be a priority, not an afterthought.

Preserving healthcare freedom is one of our core values, and at the forefront of everything we do.

That’s why we are the leading independent health benefits broker firm in the country when it comes to health sharing: Health sharing plans put you back in control of choosing your doctor, nationwide.

Unlike the health maintenance organizations (HMOs) and preferred provider organizations (PPOs) that dominate the Obamacare exchanges, health sharing organizations in Washington, D.C. generally do not restrict patients to in-network providers.

Instead, health sharing plan members have much greater freedom to choose their own doctors and provider

Is Health Sharing Right for Your Business?

Every business is different.

Choosing the best possible plan, whether it’s a healthsharing approach or a traditional group health insurance plan, take some careful analysis.

The good news is, it’s easy for business owners in Washington, D.C. to get a full case analysis and recommendation specific to your organization and workforce.

Just click here to schedule an appointment with one of our experienced Personal Benefits Managers, and we’ll start the process.

In most cases, switching to health insurance will save thousands of dollars per covered employee. But health sharing may not be indicated if you have workers with pre-existing conditions.

The consultation and analysis is always free.

Health Reimbursement Arrangements for Washington, D.C. Small Business Health Insurance

In addition to health sharing plans, there are a few other alternative health insurance options for small businesses in Washington, D.C. These include:

- Health reimbursement arrangements (HRAs) HRAs are employer-funded accounts that employees can use to pay for health care expenses.

- Health savings accounts (HSAs) HSAs are tax-advantaged accounts that allow individuals to save money for future medical expenses.

- Direct primary care (DPC) plans DPC plans are a type of healthcare delivery model that emphasizes primary care and preventive care.

HRAs are a tax-free way for employees to save money on their health care costs.

HSAs can be used to pay for deductibles, copays, and other out-of-pocket costs.

DPC plans typically offer lower costs than traditional health insurance plans and may provide better access to care.

It is important to weigh the pros and cons of each option carefully before choosing the best health insurance plan for your small business.

QSEHRAs—The HRA for Small Businesses

For small businesses with fewer than 50 full-time employees, there is a special type of HRA called the Qualified Small Employer Health Reimbursement Arrangement, or QSEHRA.

This program is designed to help small businesses provide health insurance options for their employees without having to offer an expensive traditional group health insurance plan.

With a QSEHRA, your business gets out of the health insurance game completely, and instead reimburses workers up to a cap to buy their own qualified health plan.

To start a QSEHRA plan, you must not currently offer a qualified group health insurance plan to your employees, or you must cancel your current group insurance plan when you implement the HRA.

When you cancel your health insurance plan and replace it with an HRA, your employees will qualify for a Special Enrollment Period.

This is a 60-day window during which your workers can purchase their own ACA-qualified insurance plan with guaranteed issue rights, without going through medical underwriting.

This helps ensure your employees don’t face a break in coverage when you drop your group health insurance plan altogether and replace it with a QSEHRA.

With a QSEHRA, businesses can set their own contribution limits,

For 2024, the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) limits are as follows:

- Single Coverage: Employers can reimburse up to $5,850 per year for employees with individual coverage.

- Family Coverage: For employees with family coverage, the reimbursement limit is up to $11,800 per year.

These limits are adjusted annually for inflation by the IRS and are designed to provide small employers with a flexible option to offer health benefits to their employees.

Employees can then use the money in their QSEHRA to purchase health insurance on their own through Healthcare.gov or a private broker. This preserves their eligibility for subsidies that they would not receive if they were covered under an employer-sponsored group health insurance plan.

As an employer, you can choose to reimburse your employees for their health insurance premium only, or for their premiums plus additional medical expenses.

HRA Advantages

There are many advantages to Health Reimbursement Arrangements (HRAs).

Money you spend on HRA benefits for your employees is fully tax deductible to you, as well as tax-free to your workers.

You retain control of HRA money until it’s actually disbursed to workers. It remains available to you as operating capital. You don’t have to deposit it with any third party.

Employers have a great deal of flexibility in designing their own HRA benefits, including what expenses you are willing to reimburse.

Workers don’t lose health insurance coverage if they leave the company, or change to contractor status. With the QSEHRA approach, the worker owns his or her insurance policy, and controls it. Not the employer.

The Direct Primary Care Advantage

Direct primary care (DPC) is a healthcare model where patients pay a monthly fee to their doctor for unlimited access to basic primary care services.

There are no deductibles, copays, or coinsurance costs to see your direct primary care doctor. DPC doctors generally do not take insurance at all (some will take Medicare patients).

This enables DPC practices to save a fortune, because they don’t have to maintain large teams of people who do nothing all day but bill insurance companies.

This can save patients a lot of money on healthcare costs, especially for those who frequently see their doctor, and those who have small children.

DPC works because this model allows doctors to take on much smaller patient loads than in traditional fee for service practices. They can therefore spend much more time face-to-face with each patient, resulting in a much better healthcare experience for both patient and physician.

In addition to saving money, DPC can also improve the quality of care. Because patients have more time with their doctors, and they can build a relationship with their doctor over time. This can lead to better communication and care, which can improve health outcomes.

Some other advantages of DPC include:

- Greater access to physicians

- More personalized health care

- More preventive services

- No additional cost sharing

- Shorter or non-existent wait times

- Email access to doctors

- Easy access to doctors via telemedicine

- House calls (in some cases

What Services do DPC Physicians Provide?

Direct primary care (DPC) doctors provide a range of services, including:

- Unlimited office visits

- Preventive care

- Chronic disease management

- Treatment for acute illnesses

- Basic pediatric services

- Telehealth and mental health services

- In-office procedures

- Wellness guidance

DPC doctors may also offer extended appointment times and 24/7 access.

Some services that DPC doctors typically do not cover include:

- Emergency care

- Hospitalization

- Specialist care

- Prescription drugs

If you are looking for a more affordable and convenient way to access healthcare, DPC may be a good option for you.

Learn More: Why Smart Employers Are Dropping Health Insurance for Individual HRAs + DPC

Level Up: Combine DPC With Health Sharing

One of the biggest advantages of combining DPC with health sharing is that you don’t have to pay twice for the same service.

Health sharing plans typically don’t share costs for routine primary care services. Instead, they focus on sharing the costs of more expensive care.

This means that you can use your health sharing plan to cover the costs of specialist visits, surgeries, and hospitalizations, while you use your DPC plan for your routine care.

By combining DPC with health sharing, you can get the best of both worlds: high-quality primary care and affordable coverage for more expensive care. You’ll also save money by not having to pay twice for the same service.

LEARN MORE: The DPC DIRECT Health Sharing Plan Is Designed Specifically for Direct Primary Care Patients

Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) can be a great way for employees to save money on their medical expenses, and they can also help to lower the cost of employer-sponsored health insurance plans.

HSAs allow individuals to set aside federal pre-tax money to save for future medical costs. Both employees and employers can contribute to HSAs, and the money in an HSA grows tax-deferred. Withdrawals from an HSA are tax-free as well, as long as they are used to pay for qualified medical expenses.

In Washington, D.C., employer contributions to employees’ HSAs are fully deductible under federal income tax. However, Washington, D.C. does not allow HSA deductions for state income tax purposes.

HSAs are a great option for Washington, D.C. residents and businesses looking for ways to save money on health care costs.

Can I combine HSAs with health sharing?

The HSA SECURE plan is a specially-structured health sharing plan that preserves an employee’s eligibility for pre-tax contributions to a health savings account.

This is a great way to combine the tax and healthcare advantages of a health savings account with the cost-saving advantages of health sharing.

However, in order to enroll in the HSA SECURE plan, your employees must have some self-employed or small business income or ownership. If your employee or their spouse has any small business, freelance work, or side hustle of their own, and they are in good health with no preexisting conditions that need ongoing care, the HSA SECURE plan could be a great option.

The HSA SECURE plan may also be a great money-saving option for you and your partners as a small business owner. Your employees would have to enroll in HSA SECURE on their own, but once they’ve enrolled and established an HSA, you can make pre-tax contributions to it on their behalf, up to the annual limit Congress establishes each year.

Click here to learn more about HSA SECURE

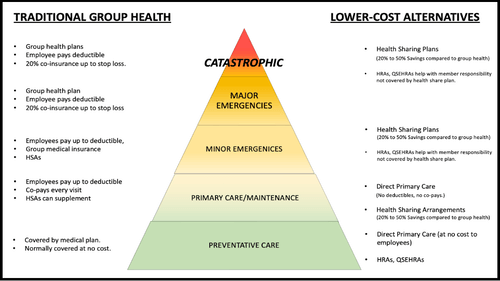

Plan Design: Address All Levels of the Care Pyramid

A quality employee health benefits package should encompass all aspects of the Employee Healthcare Pyramid as shown below.

The Employee Health Care Pyramid depicts the entire spectrum of care from basic preventive services to primary care for maintenance and early detection of health issues, and finally, coverage for catastrophic events.

This ensures that employees have access to the care they need when they need it, without having to worry about the cost.

The Employee Healthcare Pyramid

As shown in the below diagram, a good employee health benefit package should cover all levels of the Employee Healthcare Pyramid, from routine preventive health care to primary care for maintenance, early detection of health issues, and catastrophic incidents.

On the left of the diagram, you’ll find common traditional insurance-based solutions that address each level of the pyramid. On the right, you’ll find a number of alternative, more affordable approaches to providing meaningful protection for employees at each respective level.

It’s important to have a good plan design that provides employees with affordable solutions at each of these levels. This helps ensure that no employee has to delay or go without care because they can’t afford a premium, coinsurance, or copay.

Your Personal Benefits Manager can help you create a custom plan design for your workforce that provides a solution at each level of the Care Pyramid—often at a fraction of the cost of a traditional group plan to the employer.

Read More About Group Health Insurance Options in Your State

What to Do Now?

The best course of action is to gather your employee census and contact HSA for America to receive a free, no-obligation business health plan analysis and recommendation.

Our team of experienced Personal Benefits Managers will work with you to understand your workforce, budget, needs, and any preexisting conditions to design a plan that meets the unique needs of your company. We’ll help you stay competitive and attract top talent while providing your employees with the quality care they deserve.

For Further Reading

HRA For America Saves Small Businesses Thousands in Healthcare Costs

How To Compare Health Sharing Programs and Limitations: A Comprehensive Guide

Health Sharing for Small Businesses: What Business Owners Need to Know

Available Plans | HSA Info | Healthshare Info | FAQS | Blog | News | About Us | Contact Us | Privacy Policy | Agents Needed

Contact Information:

1001-A E. Harmony Rd #519 Fort Collins, CO 80525

800-913-0172

info@HSAforAmerica.com

Disclaimer: All information on this website is relayed to the best of the Company's ability, but does not guarantee accuracy. Information may be out of date. The content provided on this site is intended for informational purposes only and does not guarantee price or coverage. This site is not intended as, and does not constitute, accounting, legal, tax, and/or other professional advice. Determination of the actual price is subject to the Carriers.