New Mexico Small Business Health Insurance Options

The Complete New Mexico Small Business Health Insurance Guide (2026 Edition)

HSA for America’s Complete Guide for New Mexico Small Business Health Insurance is now available. This guide is for New Mexico-based companies with less than 30 employees. This document was created to guide small businessrs, freelancers, and independent professionals in providing their employees with health care benefits that are cost effective. It is possible to stay competitive without sacrificing the overall benefits package and compensation you offer.

New Mexico Small Business Health Insurance Health Benefits

New Mexico offers small businesses a wide range of choices when it comes time to provide health benefits to their employees.

It is the most cost-effective option to have a traditional health insurance group plan.

Prices differ by age. But according to statistics from the Kaiser Family Foundation in 2021 the cost of a group health plan sponsored by an employer that covered a worker with a family averaged $22,094, or $700 over the average.

New Mexico employee’s average contribution to health insurance is more than six thousand three hundred forty dollars, approximately 160 dollars above average.

New Mexico firms also have a number of options to choose from that may help them reduce costs. These options include:

- Health savings Accounts

- Healthcare reimbursement arrangements (HRAs)

- Direct Primary Care Memberships

- Use health-sharing programs

Your best option for small businesses will vary depending on several factors. These include the size of your firm, your budget available, as well as your workers’ age and any medical needs.

Read on the go, download our Complete Guide To Small Business Healthcare Plans.

Request a Group Quote for Your Company

New Mexico Small Business Health Insurance Geographic Considerations

New Mexico has a unique health care environment, including both the urban areas like Roswell and Santa Fe, and more rural places around Chama and Alamogordo.

New Mexico’s business owners must consider carefully how they distribute their workforce throughout the state. Executives in Albuquerque who are based at the company’s headquarters may not be able to justify choosing an HMO which restricts employees to only seeing doctors in their network when many of their workers live in Moriarty and have jobs there.

New Mexico Small Business Group Health Insurance

New Mexico’s employers most commonly choose the traditional health group plan.

Also, it’s the most costly.

What’s the process?

Employers contract with third-party insurers, who are usually profit-driven corporations. They provide a package of benefits to their employees as well as – if so desired by the employer – also to their families.

All employers that have at least 50 employees are required to offer ACA qualified health insurance for all their employees who work over 30 hours a week. If they don’t, then the employer will face a fine.

It must provide the minimum essential coverage (MEC), as required under Affordable Care Act. They are:

- Patients can receive ambulatory services without needing to go into hospital.

- Emergency Services

- Hospitalization can include overnight hospitalizations and surgery.

- The care of newborns, pregnant women, and mothers (both before and afterwards)

- Treatment for substance abuse disorders, mental illness, and behavioral problems (including counseling and therapy)

- Prescription drugs

- The Rehabilitation and habilitative Services and Devices (services and equipment to assist people with disabilities or injuries gain mental and physical abilities)

- Laboratory services

- Chronic disease management and prevention services

- Adult dental coverage and adult vision insurance are not considered essential health benefits.

Furthermore, the ACA mandates that insurance policies cover contraception and breastfeeding.

Although traditional health insurance may be the most expensive choice for your business, you will have guaranteed enrollment.

When a worker enrolls for health insurance during a period that is triggered either by their first eligibility period or a period of special enrollment due to an eligible life event (or during the November 1st open enrollment), the insurance provider cannot refuse them coverage because of medical issues.

Small business Owners in New Mexico Are Not Required To Carry Health Insurance

The Affordable Care Act does not require employers to provide health insurance for employees with fewer that 50.

New Mexico’s state law also does not require health insurance. It is not required to offer any health coverage if your company has fewer that 50 employees.

There is no penalty.

Employers of all sizes should consider offering health benefits. That includes very small companies. Without them, it could be harder to hire and keep quality employees.

New Mexico in particular is an attractive place for employers to find talent, since unemployment rates are low.

New Mexico employers have the potential to save lots of money by offering an employee health and medical plan.

New Mexico Small Business Health Insurance HRA Alternative

You can also offer your employees a QSEHRA (Qualified Small Employer Health Reimbursement Arrangement) that allows them to pay their individual health insurance tax free.

Employers can benefit from QSEHRAs in the following ways:

1.) Contribution limits are not applicable

QSEHRAs don’t require a set minimum annual contribution, unlike pension plans. You can set up your budget and adjust it each year based on your cash flow.

You can control your budget for health care benefits with a QSEHRA.

2.) Flexibility

It is possible to offer different amounts based upon the employee’s marital and family status. It is possible to discriminate and offer a bigger benefit for employees with children than those who do not have any.

3.) The tax exemption is available to both employees and employers

You can deduct your contributions as compensation expenses. Contrary to cash compensation, employees do not have to pay taxes on QSEHRA benefits as long as they keep a health plan with the minimum coverages required by the Affordable Care Act.

In this case, a QSEHRA will be more effective than just offering employees a health insurance allowance that they can use for other purposes or to pay their health insurance premiums.

4. QSEHRAs are designed to support employees’ choice

In many cases, traditional health plans for groups limit their options to one or just two. This is unfair because employees are often in very diverse situations.

These products are frequently overpriced and ill-suited to the needs of workers because they were chosen by company managers and HR, rather than by workers.

QSEHRAs offer workers and their families more options, allowing them to find the plan that best suits them.

New Mexico’s Taxation of Employer Health Benefits

Under federal and New Mexico legislation, the premiums for health insurance you pay are completely deductible as a business cost. Employees do not pay taxes on them.

The overall cost of healthsharing plans is lower. Employees can deduct the monthly costs. Employer assistance in paying for health-sharing costs is taxable.

New Mexico Small Business Group Health Insurance: Disadvantages

Employers and employees alike have some serious disadvantages to the traditional employer-group health insurance.

- Cost

We have already mentioned that the cost to provide health insurance is high. This can be especially true for industries with high labor costs.

Many workers are overburdened by the requirements and coverages mandated in health insurance plans. Washington, Santa Fe and other government agencies have done this.

According to traditional health plans, carriers must also include benefits such as mental and drug addiction coverage. They may even charge for maternity insurance. But many employees don’t require or want these.

This reduces their efficiency and costs.

- Inflexibility

Most group insurance programs offer an all-encompassing strategy which does not necessarily meet specific needs and budgets of employees. By their nature, employer-sponsored plans for group health care tend to have only a couple of options. These may not meet the specific needs of employees.

It may make sense for workers to buy their own plans on the market. They could take advantage of any subsidies provided by the Affordable Care Act.

A less expensive plan of health sharing, as discussed in the following paragraphs, may suit them better. The innovative, affordable and flexible alternatives to traditional health insurance are a good solution, especially for healthy workers without pre-existing medical conditions. Below, we discuss health sharing plans in greater detail.

The following sections will discuss in detail health sharing plans.

- Administrative burden

A full-fledged healthcare benefit comes with substantial administrative expenses. As part of this, you will be responsible for managing the documentation, ensuring compliance with plans, preventing non-qualified employees from enrolling in them, and answering staff questions. The health insurance program within an organization must run efficiently and smoothly.

However, they are an enormous burden on very small businesses who lack the manpower to hire a HR department to administer the plan.

They are a burden for very small companies who do not have enough employees to support a full time HR team to manage the plan.

Some business owners use other strategies, such as the Health Care Stipends or Reimbursement Arrangements.

New Mexico Health Sharing Plans

Small businesses in New Mexico can benefit from health sharing plans as an affordable and viable alternative to expensive insurance.

Medical cost-sharing plans are becoming a popular alternative to traditional group insurance in New Mexico. They offer a more affordable option. Companies can save as much as 50% by switching to health-sharing plans from traditional group insurance.

New Mexico’s small businesses can save upwards of $10,000 per employee annually on coverage for a family, and over $3,500 each per employee annually for a single policy.

These programs represent a revolutionary method of financing healthcare. This allows companies to afford high-quality healthcare for their staff while also controlling expenditures. A health sharing program is based on sharing resources across a number of individuals and organizations.

As an alternative to traditional health insurance which requires paying premiums, Health Sharing Programs allow participants to make a set amount of cash per year.

Health Sharing Plans vs. Health Insurance

A health-sharing plan is different from a medical insurance.

In contrast, healthsharing ministries are non-profit associations that bring together people of similar minds to share in the costs of medical care. Contrary to most health insurance providers, who are for-profit companies, healthsharing ministries are nonprofit.

Mandatory Coverage

Health insurance plans are not required to meet these requirements. Health sharing organisations are exempt from the 10 Minimum Essential Coverage requirements.

The cost of treatment for drug addiction is not covered by medical cost sharing plans for those who do never take drugs. The plans do not have to cover injuries that result from drunk driving.

When there are pre-existing conditions

The waiting period for healthsharing plans is usually longer than traditional insurance. They may also require a certain number of months before the plan will pay out on pre-existing condition treatment.

They also often impose waiting period for surgery except for those injuries or accidents which were unforeseeable at the time the member enrolled.

They help to eliminate a large amount of adverse selection. And they allow health sharing organisations to provide a set of excellent benefits at a fraction their cost compared with a policy purchased through beWellnm or an ACA-qualified, unsubsidized group health insurance.

Please note that healthsharing plans do not qualify for subsidy under the Affordable Health Care Act. However, the savings are so significant that even those who do not qualify for subsidies can benefit by switching to a healthsharing plan.

New Mexico employers may find it more beneficial to switch from small group insurance plans that receive a subsidy on premiums under the ACA.

Request a Group Quote for Your Company

Health Sharing and Network Restrictions in New Mexico

Health sharing plans offer greater choice in healthcare providers than traditional managed care plans like HMOs or PPOs. These are the two most popular employer sponsored group health insurance policies.

Most healthsharing organizations New Mexico does not limit patients to only in-network providers. Members of health-sharing plans can select their doctor. People should be able to choose the doctor they want.

Are you a business that can benefit from health sharing?

Every business differs. An analysis is required to determine the best option for your company, whether that’s healthsharing or a more traditional plan.

You can get full analysis of your case in New Mexico and receive recommendations tailored to you and your team.

You can make an online appointment by simply clicking on this link.

And If you’ve prepared a census of your employees, it will make things easier.

Switching from medical insurance to other types of coverage can often save employees thousands. If you are dealing with employees who have pre-existing health conditions, it may be best to avoid health sharing.

It is free to consult and analyze.

Small Businesses in New Mexico can now get health reimbursements

HRAs are tax-free benefits funded by employers that reimburse employees for their individual health care costs.

New Mexico’s small business owners often do away with the benefit of group insurance. They establish a HRA instead, which they use to give workers cash for them to purchase their own individual insurance with pretax dollars.

It allows employees to benefit from available subsidies, further reducing net costs both for the employee and company.

Employees can access their HRA benefits if any money remains after the payment of premiums. This includes prescriptions for durable medical equipment and prescriptions. HRAs benefits are again tax-free.

When you offer an HRA as a replacement for formal group health coverage, employees have the option to pick and choose health insurance that meets their individual needs.

Please click here to learn more about HRAs for your business.

HRAs for New Mexico Small Business Health Insurance

QSEHRA or Qualified Small Employee Health Reimbursement Agreement (pronounced “Cue Sarah”) is the special HRA type that small businesses can utilize.

This benefit is intended for businesses with less than or equal to 50 full-time staff members, who are not offering a standard group health care plan.

The QSEHRA allows businesses to choose their maximum QSEHRA contribution, subject to certain restrictions. New Mexico employers may contribute $5,850 to individual employees up to $487.50 a month and $11,800 to employees with families up to $983.33 a month as of 2023.

They can use the money they receive to buy insurance for themselves via an online insurance exchange, or via a Individual Benefits Manager. They can still qualify for the subsidy if they purchase their own insurance through an online health insurance exchange or a Personal Benefits Manager in the individual and family market.

If you are the employer, then you have two options: You can either reimburse your employee’s health insurance premiums, plus any medical expenses, or just their premiums.

Special Enrollment periods for QSEHRAs

You will have to offer your workers a Special Registration Period if your HRA replaces your old health insurance. It is a window of 60 days during which employees can buy their own ACA-qualified health insurance with guaranteed issues rights without having to undergo medical underwriting.

If you decide to replace the existing health insurance program with a QSEHRA, this will make sure that none of your employees lose coverage.

HRA Advantages

Health Reimbursement Arrangements have many benefits.

You can deduct the money that you pay for HRAs, and your employees will not be taxed.

HRA is your money, and you retain it until the funds are actually distributed to the workers. This money remains in your account as an operating capital. No third parties are required.

With HRAs flexibility, they can be designed in many different ways by employers. This includes the expenses that you want to reimburse.

Also, the workers’ health coverage is not affected if they change their status to contractor or leave the organization. The QSEHRA allows the employee to control their insurance. The employee, not the employer, owns their own policy.

HRA Disadvantages

Many workers do not wish to take on the task of researching and selecting their own healthcare plan. Some workers need assistance to help them navigate through the change.

We can help if you are in this situation. There is no one left behind.

Call 800-913-0172 or have your workers simply click on this link for an appointment to receive personalized service.

Click on here to find out more about the alternatives offered by New Mexico’s small businesses to health insurance sponsored by their employers.

Direct Primary Care Benefit

Direct Primary Care plans, or DPC, are an alternative model of healthcare that have gained in popularity throughout the US and New Mexico.

The model is membership based. For an affordable flat-rate monthly fee (similar to that of a gym), your employees get as many visits they need in person, or via telehealth.

DPC’s monthly membership fees start at just $80 and are a viable option for people to take care of their health, without having to pay copays or insurance.

DPC plans offer members unlimited access for routine primary, chronic, and preventive care.

Some of the services that are commonly offered by primary direct care include:

The following are some medical services provided by direct primary care doctors.

- Preventive care. DPC doctors are committed to preventive care and offer routine screenings, immunizations and checkups.

- DPC Doctors treat injuries, illnesses, and infections such as minor cuts, skin diseases, and colds.

- Management of Chronic diseases DPC doctors assist patients in managing chronic conditions such as hypertension, diabetes, arthritis and more. These doctors offer ongoing treatment, monitor patients, and adjust their plans of care as required.

- Comprehensive physical exams. DPC doctors provide comprehensive physical examinations in order to identify and assess risks as well as personalize health recommendations.

- Urgent care. DPC is often able to offer same-day, or the next-day, urgent care.

- The appointment system allows patients to be seen quickly for medical problems that are not emergencies.

- Laboratory and diagnostics services. DPCs may perform or arrange a range of lab tests including X-rays/ultrasounds/electrocardiograms.

- Management of medications. DPC Doctors can prescribe medications. Monitor their effectiveness. And make any adjustments needed. Additionally, DPC doctors provide medication education and counselling.

- Mental Health services DPC practices offer a wide range of mental health treatments as part their total care. DPCs may also refer their patients to a mental health specialist when they need it.

- Minor procedures. DPCs are equipped to carry out minor surgeries in their own offices.

- Care coordination and referrals. DPC’s doctors coordinate and advocate for their patients, including coordinating with specialist physicians, hospitals and healthcare providers.

As there is no insurer involved, no copays are required. All costs are covered in the subscription fee. Cash-strapped people can get immediate access to the health care they deserve. No longer will they have to wait until later because the deductible and co-pay are too high.

In order to get coverage for services that DPC does not cover, patients may choose from supplemental plans like high-deductible plans, accident insurance or health sharing plans. DPC’s membership already includes routine care, so patients are able to choose more affordable coverage, like healthsharing, than traditional health insurance.

Accounts for Health Savings (HSAs)

The HSA (Health Savings accounts) is a powerful tool that can assist workers in managing their health care costs and also help to keep the premiums of workplace health insurance lower.

New Mexico business and resident alike need as many tax benefits as they can. New Mexico corporations can deduct employer contributions into employees’ Health Savings Accounts as compensation.

HSAs enable individuals to pre-tax funds for future medical needs. HSAs can be funded by employees as well as employers. However, the annual contribution limit is set each year by Congress to match inflation.

HSAs offer tax-deferred earnings on money and withdrawals for qualifying healthcare expenses.

New Mexico Small Business Health Insurance HSA Qualifications

To qualify to make contributions or enjoy pretax employer contributions, an employee must sign up for a high-deductible plan.

IRS definition of a High Deductible Health Plan for 2023 is any plan which has a deductable at least $3,000/$1,500 for family plans.

A HDHP can only have a maximum of $7,500 in annual out-of-pocket expenditures (including deductibles copayments coinsurance. This limit is for individuals and it’s $1,500 for families.) It does not include out-of network services. ).

What if I want to combine HSAs or health shares?

At present, there is only one plan that allows employees to contribute pre-tax money into a Health Savings Account: the HSA Secure Plan. It’s available via HSA For America.

HSA SECURE Plan offers a great way to combine tax advantages and savings on healthcare with health sharing.

Your employees will need to have a self-employed income, or be a business owner, before they can enroll.

In order to be eligible, the employee must earn income as a sole proprietor or own a small company.

HSA SECURE will not be available for straight W-2 workers. HSA-SECURE may work for you if the employee has a side business, freelancing, or a freelance gig and is in excellent health.

As a small business, you may want to consider the HSA-SECURE Plan as an option that can save both your and partners money.

HSA SECURE is only available to employees who enroll on their own. If they already have an HSA established, then you can still make pretax contributions on their behalf up to the limit Congress sets each year.

How Are New Mexico Small Business Health Insurance Benefits Taxed?

You now know about the different strategies that small businesses can use to supplement traditional health coverage. Below is a quick table describing how taxation works for each benefit.

| Plan Type | Employer | Workers |

|---|---|---|

| Traditional health insurance premiums | Tax deductible. May qualify for a tax credit (see below) | Non-taxable |

| HSA contributions | Tax deductible | Pre-tax, up to certain limits. No income limitations. |

| Health sharing costs | Tax deductible as a compensation expense | Taxable as ordinary W-2 income |

| Health reimbursement arrangements | Tax deductible | Benefits are non-taxable to the employee |

| HSA withdrawals | N/A | Withdrawals for qualified medical expenses are tax-free. Otherwise taxable as ordinary income. A 20% penalty for non-qualified withdrawals applies up until age 65. |

| Direct primary care costs | Tax deductible as a compensation expense | Taxable to the employee |

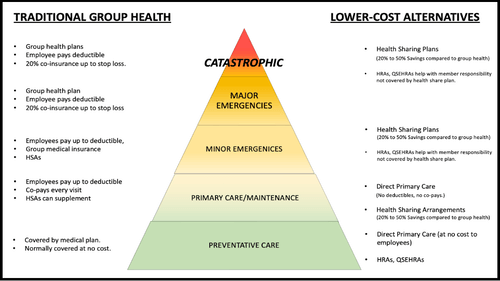

New Mexico Small Business Health Insurance Pyramid: Addressing All Levels

As shown in the below diagram, a good package of employee benefits should cover all the levels of the Employee Healthcare Pyramid, from preventative care to primary care for early detection and maintenance of health issues, up until catastrophic events.

On the left, you will find a list of common solutions based on traditional insurance that can be used to address the different levels of the Care Pyramid.

While on the right, you will find a list of more affordable alternatives to offer meaningful protection at every level of Pyramid.

Plan design that is good will offer employees affordable solutions on each of these levels. The plan should ensure that none of the employees are forced to postpone or skip care simply because they don’t want to pay a higher premium or for coinsurance.

The Personal Benefits Coordinator can create for you a unique plan which provides solutions to each of the levels of the Care Pyramid. This is often done at a fractional cost compared to a conventional group plan.

New Mexico Small Business Health Insurance Tax Credit

Small Business Health Care Tax Credit, passed with the ACA allows certain small businesses claim a federal credit up to 50% on their employees’ health insurance costs.

This program is designed for small business owners who have 25 or less employees and tend to hire workers at lower wages.

The credit is available to both for-profit companies and nonprofits.

* Has fewer then 25 employees. Average salaries are around $53,000. It is not common to include owners when calculating average salaries and the number of workers in a company. Also, employees are counted as “full-time counterparts” (FTE). The two part-time employees will equal the full-time equivalent.

* Employers must cover at least 50% the costs of insurance premiums.

The state exchange in New Mexico is beWellnm.

When an employer has at least 25 employees and/or a wage average of more than $53,000, they are no longer eligible for the tax credits.

What if I do not owe any tax this year? Am I eligible to receive the tax credit if I don’t owe any?

Yes. You can carry back the tax credit to use it to offset the income tax liability for the year before or you can carry forward the tax credit to offset the liability over the following 20 years.

This credit is refundable for businesses that are exempted from paying taxes.

To learn all about the Small Business Health Care Tax Credit consult your tax professional.

Combine New Mexico Small Business Health Insurance Plan Strategies

When it comes to maximizing your coverage, combining different programs is a wise move.

Combining several health insurance packages can help employers control costs, while providing coverage to employees.

You could combine Direct Primary Care Plans (DPCs), for the normal care of primary patients, with health plans that are low-cost and cover catastrophes.

This alternative to traditional group health insurance can make it more affordable, either for the company or for employees.

Giving employees the opportunity to select between an HDHP HDSA plan and a health-sharing plan as well as the ability to contribute money into a Health Savings Account can provide them with more freedom, while potentially lowering costs.

Now What to Do?

For the best results, you should conduct an employee survey and Contact Us. We will provide a complementary analysis of your business’ health plan.

Many of PBMs who work for us have also been entrepreneurs themselves. Since they have been business owners, our PBMs know how important it is to hire and retain talent that will help your company remain competitive.

A Persona Benefits manager from HSA for America will be assigned to you. This persona benefits manager will talk to you about your staff and their families, discuss your needs and budget, assess your employees’ contributions and take into account any existing health conditions.

Do I have to offer health insurance AND health sharing together?

It is possible to offer the two options together, giving employees the choice of which option best meets their needs.

It is important to note that if the number of employees who opt out from a health plan for a company falls below the minimal participation required, then a policy cannot be maintained. However, an HRA can be used to reimburse your staff for personal health insurance. The cost will be similar.

New Mexico Small Business Health Insurance: Frequently Asked Questions

How do health sharing plans and insurance for small business differ?

While health insurance plans are offered by traditional insurers, healthsharing allows members to contribute money to an account that covers each others’ medical expenses.

New Mexico: Can contributions by employers towards HSAs qualify as state tax deductions?

Yes. New Mexico deducts employer contributions toward employee HSAs from its state income tax.

Offer Direct Primary Care Plan (DPC), alongside other coverage choices, make sense to small business in New Mexico?

Combining DPC plans with lower-cost health coverage, like Health Share Plans, provides comprehensive and affordable healthcare solutions for both small businesses and employees.

Is it possible for a New Mexico-based business to still receive the Small Business Health Care Tax Credit even though they do not owe New Mexico tax?

If a company does not have any tax obligations in one year, they can use the Small Business Health Care Tax Credit as a way to pay back their income tax for the year before or carry it forward to the next 20 years.

HRAs are they compatible with health-sharing plans, individual insurance plans and other types of coverage?

HRAs may be combined with other options of coverage. HRAs are used by some small companies to reimburse their employees for the premiums of individual health policies. HRA money can’t be used for reimbursements to employees.

How do I know which health insurance options and cost-sharing plans are best for my New Mexico business?

It’s not worth it to go at it alone. Talk to an Employee Benefits Manager. He or she can perform a free assessment and provide recommendations, based on specific requirements, your budget, the employee population, and other factors. You can work with them to design the best plan possible that will benefit your employees and keep you competitive.

Does health sharing have a waiting period on conditions pre-existing?

It is possible that some plans require a certain waiting period before beginning coverage for conditions already present. If you want more information about a specific plan, review the guidelines of that plan or contact a Personal benefits manager.

Health Savings Accounts can be used to help New Mexico workers manage medical expenses. It enable individuals to pre-pay for medical expenses in the future. Employers and employees both can contribute. This provides tax advantages as well as potential savings in healthcare expenses.

New Mexico employers can contribute to HSAs for their employees.

The annual contribution limits set forth by Congress apply to employers who wish to contribute to HSAs for their employees.

How can I get the Small Business Health Care Tax Credit (SBHCTC)?

Tax credit claims can be made on Form 8941 of the IRS for businesses that are for profit, whereas small tax exempt businesses will need to submit Form 990T.

HSA for America doesn’t provide tax advice. To get the full details on how to claim this credit, employers are advised to consult with their tax advisor.

Does New Mexico cover the cost of maternity care under health sharing plans?

New Mexico has a number of plans, including health insurance and healthsharing, that cover maternity services, such as prenatal care, labour, and postnatal treatment. There are some plans that restrict how much a child’s cost sharing benefits can be shared if they were conceived out of marriage.

What is the maximum size for small businesses that can apply to these programs in New Mexico?

QSEHRAs (Qualified Small-Employer Health Reimbursement Arrangements) are available exclusively to employers with fewer that 50 employees. Other HRAs are available if your company has over 50 employees.

A requirement of the ACA is that employers must provide a qualifying health insurance plan to their employees. If they do not, they will have to pay a fee. Consult your Personal Benefits Specialist if, within the next year, you will be hiring the 50th worker full-time or its equivalent. The plan that you design could change.

Read More About Group Health Insurance Options in Your State

Available Plans | HSA Info | HealthShare Info | FAQS | Blog | News | About Us | Contact Us | Terms & Conditions | Privacy Policy | Agents Needed

Contact Information:

1001-A E. Harmony Rd #519 Fort Collins, CO 80525

Disclaimer: We work hard to keep this information accurate, but we cannot guarantee it. Information may be out of date. We provide this content for informational purposes only and do not guarantee price or coverage.

We do not provide accounting, legal, tax, or other professional advice on this site. Determination of the actual price is subject to the Carriers.

© 2026 - All Rights Reserved